forensic analysissecurities · money-laundering corpus

Follow the Stock

The Anatomy of a Decades-Long Stock-Laundering Pipeline

How attorney Kyleen E. Cane issued private stock to herself and family, ran it through four corporate shells — Tele-Lawyer → Dynamic / LATI → MW Medical → Davi Skin — wrapped each shell around entities that handled federal money, changed her own legal identity to break the paper trail, then sold the stock through CEDE & Co. street name and four Bermuda nominees, liquidating $6.39M offshore below every disclosure threshold. The pipeline ran from a 29 Dec 1995 Nevada incorporation to the 2008 offshore sale, with the concealment — backdated filings, swapped identities, a renewed judgment — still running in 2023: a quarter-century enterprise.

Read this first. What follows is not a simple theft. It is a sophisticated securities-fraud and stock-laundering scheme whose moving parts span five professional disciplines at once — securities law, corporate bankruptcy, federal tax and FBAR reporting, offshore private banking, and SEC disclosure mechanics — engineered so that no single regulator ever sees the whole. Following it takes a working grasp of each. The cards below make the machine legible; the full securities-fraud primer explains every concept in plain language.

The thesis, in one sentence. A corporate securities attorney sits at the center as the kingpin of a shell factory — using the trust and access of securities-counsel services to launder private stock into tradeable public shares, loot the corporate assets of the companies she takes over, and defraud the entrepreneurs who hired her — while the offshore proceeds are kept beyond the reach of the IRS. Every concept here, and every section that follows, is a part she pulled to make that work.

Five plain-language concepts make this fraud legible — for judges, investigators, and the public. Each is a lever the enterprise pulled in turn.

CEDE & Co. / DTC

CEDE & Co. is the nominee of the Depository Trust Company — the world's largest securities depository ($50T+). Brokers hold your beneficial interest; DTC holds the master certificates. A "deposit" converts a paper certificate into tradeable book-entry form. Depositing 36 sequential certificates (2029–5323) made private, hidden stock publicly sellable; the sequence proves a single controlled source.

CUSIP

A CUSIP is the 9-character "fingerprint" of a public security. It turns stock into an official asset class institutions and foreign entities can hold. Running worthless private Tele-Lawyer stock through public shells gave the hidden position a CUSIP — real market value with no legitimate business behind it.

Regulation S

Reg S lets issuers sell to foreign investors without SEC registration; the shares resell into the U.S. after a holding period. The abuse: transfer stock to offshore nominees in Bermuda (LOM), wait out the restriction, and collect proceeds offshore, untaxed, while the shares trade freely onshore.

The shell-selling model

Why pay $250K–$500K for a corporate shell? To sell a hidden position. Swap private shares into a listed shell, then sell into the market. The seller wins twice — cash for the shell and a retained hidden position later liquidated offshore. It is, functionally, stock laundering.

Primer · concepts underlying the transformation pipeline below

✦

The Scheme at a Glance — Hover Any Step

The entire pipeline on one strip — each box is an entity or a move, each arrow is how the same insider stock travels to the next hop, ending at the terminal pump-and-dump. Hover (or tap) any box for what happened and when; hover the arrows for how the stock moved between them. The scroll-driven diagram further down walks the same chain step by step.

Before any of it can be dumped, the controlling stock has to be placed and hidden. That happens here. When Tele-Lawyer's private equity is taken public through the Dynamic reverse merger, control is split across the Cane family so that no single filing reveals the group. On 18 Jun 2001, five "independent" reporting persons file for the same issuer on the same day — each disclosing a sub-group stake, none disclosing that the five are one coordinated bloc holding 85.7%, a §13(d)(3) group required to file together. This is the seed the rest of the pipeline exists to monetize; the sections that follow show that same planted stock being re-skinned, bankrupted clean, and dumped offshore.

On a single 24-hour window, five "independent" reporting persons filed for the same issuer — each below a disclosure line, none disclosing a group. The fields that tie them to one office are bolded.

* All five statements report the same 18 Jun 2001 event, were transmitted by a single EDGAR filer (0001075793, Cane Clark), and name the Cane office as the issuer — the through-line that ties the “independent” holders to one desk.

(702) 312-6252 — Cane's law-office line is the sole notice contact on the 13D; the 13G holders list none89014 — Cane and her parents share the Henderson ZIP; "mother" Shirley Cane filed the same day312,500 — three "unrelated" holders hold the identical block, consistent with equal allotment, not market purchasesone EDGAR filer (0001075793, Cane Clark) submitted all five "independent" statementsindividual 48.7% sits just under the 50% control line; no joint-filing agreement was ever disclosed

The bloc's "Mekelburg" holders are Cane's siblings: Brian and Nancy Mekelburg appear in the family record as Brian M. Cane and Nancy M. Cane — Mekelburg is the siblings' married surname — and the Mekelburg Family Trust (executor Stuart Cane) holds more. The parents Herb & Shirley Cane filed the same day, three days after Cane herself.

Five same-day Schedule 13G/13D filings · Legal Access Technologies CIK 878146 · one EDGAR filer, one Las Vegas office

★

Davi Skin — The Pump-and-Dump

Davi Skin is where the stock was finally sold. It is the terminal entity of the whole pipeline — the public listing the laundered shares were walked toward for years, then dumped into the market. The mechanics are written in the certificate register: on 5 March 2007, certificate 5304 moved 946,085 shares — 16% of the float — into CEDE & Co. / DTC street name in a single deposit; 29 days later, on 3 April 2007, certificates 5309–5312 placed 2,295,388 shares with four Bermuda LOM nominees at exactly 3.97% each. Together the enterprise controlled 4,545,213 shares — 76.69% of the free float and roughly 89% of trading volume, liquidated across 2007–08 for $6,385,033 into Bank of Bermuda and N.T. Butterfield.

The setup, though, was years in the making. It begins where the pipeline begins: Cane issued herself the controlling block of the shell — 2,871,051 shares (48.7%) of Dynamic Associates / Legal Access Technologies in June 2001 — then spent six years concealing that ownership. The block was layered through corporate re-skins (Dynamic → MW Medical → Davi Skin, the reporting CIK travelling intact), masked behind a legal name and gender change (Michael A. Cane → Kyleen E. Cane), and finally split into DTC street name and offshore nominees — while federal filings were signed under a name that was no longer legal and the same ownership was misrepresented to courts and federal authorities. By the time the certificates were placed for sale, the controlling owner had been erased from the visible record. What follows is what was sold, and how it was placed.

The anomaly, dated — the whole scheme end to end

Every move, in sequence: how the stock was planted (private placement in Tele-Lawyer → reverse merger into Dynamic → issuance to “Michael A. Cane” → the backdated identity), how the vehicle was re-skinned (Dynamic spins out MW Medical then winds down; the MW Medical bankruptcy wipes the outside shareholders and spawns new shells; the shell is sold to Parrish and renamed Davi Skin), and how it was dumped (CEDE & Co. + LOM Bermuda placement, the Lakha-financed pump-and-dump, and litigation run to bury the records). Open the badge on the backdated-identity row to see both cached EDGAR submissions, highlighted.

29 Dec 1995Tele-Lawyer, Inc. incorporated in Nevada (C23375-1995); Cane issues the controlling block to herself and family — the seed stock, entirely outside SEC scrutiny

25 Feb 1998Dynamic Associates 8-K: spins out MW Medical, Inc. 1-for-1 to Dynamic holders (distributed 11 Mar 1998) — the reporting shell (CIK 0001059577) whose register mirrors Dynamic's

12 Jun 2001Tele-Lawyer reverse-merges into Dynamic Associates (SIC 6770 blank-check shell); a 153:1 reverse split wipes 99.35% of the float; renamed Legal Access Technologies (LATI)

18 Jun 2001Dynamic/LATI stock issued to “Michael A. Cane” — SC 13D reports 2,871,051 sh (48.7%); five same-day 13G filings hide the coordinated 85.7% family bloc

22 Jan 2002MW Medical Chapter 11 8-K — the bankruptcy that will extinguish the outside shareholders

4 Feb 2002Joint Plan of Reorganization: Wallace's manufactured $615,871 secured position; $375,000 converted → 74,000,000 shares (74.1%), leaving a $570,775.30 convertible balance riding the shell; outside equity extinguished

4 Feb 2002§1145spawns new no-op shells to traffic — MW Asia (95% Sim), MW Europe, NW S. America, MW Fitness, Microwave Debtor — sold $250K–$500K each to marks (Beardmore: $250K for MW Asia)

30 Apr 2002Dynamic / LATI winds down — after the FY2002 10-KSB the merged hub goes dark on EDGAR, the stock already moved into MW Medical

25 Nov 2003Court order D308221: Michael Allan → Kyleen Elisabeth — the actual name & gender change (~880 days after the SEC-reported date)

10 May 2004MW Medical annual meeting approves the 500-for-1 reverse split (re-concentrating the float before the rename)

19 May 2004Divorce / marital-home transfer to Susan Eiselman, recorded in Clark County — a paper split used to move assets around, the property staying under Cane's control

24 Jun 2004MW Medical sold to Parrish Medley / Carlo Mondavi cover and renamed Davi Skin (DAVN); SIC pivots to 2844 (cosmetics); Cane installed as a director (with Wallace CEO, Sim CFO)

22 Jul 2004Backdated name change wired to EDGAR — a Form 5 (and a Form 4) carry “FORMER CONFORMED NAME: CANE MICHAEL A · DATE OF NAME CHANGE: 20010628,” the wrong change date. Open both cached submissions, highlighted →

23 May 2005Davi Skin 10-QSB Reg S — units sold to four foreign investors (later challenged by SEC staff comment letters)

10 Mar 2006Pacific Stock Transfer register (baseline): 36 sequential CEDE & Co. deposits (Nos. 2029–5323) staging 2,249,825 sh into DTC street name

13 Apr 2006 · 5:10pmWallace defames Parrish Medley — she telephones and faxes handwritten notes to Davi's CFO and bookkeeper: “I find him to be a liar, a cheat, self-serving and of low moral character” — the defamation (per se / per quod) pleaded as Exhibit A

21 Apr 2006Davi Skin control litigation — Parrish Medley (the public-face CEO) sues (Medley v. Wallace; Artist House Holdings v. Davi Skin) over Wallace's concealed note, the offshore nominee structure, and the defamation; the fight is run to bankrupt the company and scatter its business records

5 Mar 2007Cert 5304 deposits 946,085 shares — 16% of float in one deposit

3 Apr 2007Certs 5309–5312 → four LOM Bermuda nominees (Arch · Hepburn · Chloe · Sunshine) · 2,295,388 sh at 3.97% each, from Wallace's $200,000 Davi note

23 Apr 2007Gunther → M.P. email: the Hepburn Holdings / Bermuda due-diligence package — the nominee paperwork behind the LOM certs

13 Jul 2007Lakha “financing” set up: a $2.2M senior secured convertible note from Amin S. Lakha (dated 13 Jul 2007; $536,163 drawn), secured by Davi's assets and convertible into shares — manufactured paper to justify issuing stock during the dump

13 Jul 2007Pacific Stock Transfer Active Shareholder Report: the offshore CEDE & Co. street-name concentration — the block staged for the ~$6,385,033 offshore liquidation into Bank of Bermuda / Butterfield

11 Sep 2007Wallace → M.P. email: an SSN request on a MetaWallet/Millicom tender pretext, routed to Cane the next day (12 Sep 2007) — a manufactured paper trail tying outsiders to the offshore structure

20 May 2008Davi Skin's last 10-QSB (filed via Baum) as DAVN collapses from $0.19 toward $0.003 — the pump-and-dump on the tape

14 Jul 2008Wallace frames K.G. — a consulting-agreement pretext to assign 556,000 shares to K.G. to issue from the transfer agent, manufacturing a placement in his name during the dump window

27 Aug 2012Davi Skin's registration is REVOKED — the shell abandoned after the offshore liquidation

Across 120 trading sessions in 2008 the close collapses from $0.19 to $0.003 while volume erupts through eleven dislocations — sessions where volume runs ≥ 3× the trailing-30 median alongside a double-digit move; one is confirmed by a control event within three weeks. Hover any bar for that day's close and volume, or tap the chart for the full pump-and-dump detail. The June–September 2007 sell-off, run through the CEDE and LOM channels, generated approximately $6,385,033 in proceeds into the Bermuda accounts before the shell was abandoned.

Certificate placement — what was staged, then sold

The certificate register records the operation in two halves. From 2004 through 2007, thirty-six sequential deposits (certificates 2029–5323) walked 2,249,825 shares into CEDE & Co. / DTC street name — the block quietly staged for sale. The placement then accelerated in the weeks before the offshore transfer: on 5 March 2007, certificate 5304 moved 946,085 shares — sixteen percent of the float — into DTC in a single deposit (→ shareholder register, CEDE & Co., p. 3); twenty-nine days later, on 3 April 2007, certificates 5309–5312 placed 2,295,388 shares with four LOM Bermuda nominees — Arch (5309), Hepburn (5310), Chloe (5311), and Sunshine (5312) — at exactly 3.97% each, a hair under the five-percent line that would have forced a Schedule 13D disclosure of identity, source of funds, and purpose. None of it was disclosed.

The same window is where the frame shows. Behind the Hepburn Holdings block, Wallace — claiming she had breast cancer — pressed the relator to serve as trustee for her daughter, drawing him into the paperwork for the Chloe / Hepburn offshore nominee. She emailed him for his Social Security number “for the form 3 filing … for your davi shares,” and, in the 2008 sale window, used a consulting-agreement pretext to harvest K.G.’s home address and Social Security number “to issue shares from transfer agent” — manufacturing a paper trail to implicate others in the offshore structure, not placing a genuine block. The record fixes the two real placements and their recipients; tying any single 2008 trading session to a specific block would take trade-level DTC withdrawal data the corpus does not hold. Every placement, filing, and email is laid out by date against the 2008 price and volume in the day-by-day chart.

The filing agent — shared, then switched at the dump

For years a single EDGAR filer — 0001255294, Cane O'Neill Taylor / Cane Clark — prepared the filings for LATI (878146), for Davi Skin and its MW Medical predecessor (1059577), and for Cane's own Schedule 13D (CIK 0001144030): the filer-agent overlap that ties the entities to one office (Cane Clark was registered agent for 202 Nevada entities). Then the fingerprint is scrubbed. Cane Clark's last Davi filing of record is 14 May 2007; the 2007 10-QSBs move to Vintage Filings (CIK 0001144204), the FY2007 10-KSB and Q1 2008 10-QSB to Baum Law Firm (CIK 0001173473 · La Jolla, CA), and — right before the July 2008 dump — to Format Inc. /FA/ (CIK 0001137091), which filed the Q2 2008 10-Q (Acc. 0001137091-08-000436, 14 Aug 2008). That filer was later renamed twice and is today Power Solutions International, Inc. (201 Mittel Drive, Wood Dale, IL 60191). LATI, after toggling agents in 2005–06, simply went dark.

precrime_score · structural risk, from EDGAR filings alone — no narrative input

The dump could have been predicted. A "precrime" model scores each EDGAR entity from its submission record alone — form types, cadence, filing agents, name history, blank-check shells, parked insider stock. By the eve of the 2007 dump, Davi Skin's lineage had already tripped a stack of these flags: a blank-check shell reverse-merged and renamed, a reporting CIK recycled through two re-skins, a manufactured Chapter 11, a single filing agent across "unrelated" issuers — then that filing agent switched right before the sale. Enough structural signal preceded the dump that the model would have flagged it.

That is the investigative lever for a regulator or government contractor: precrime can't see the off-EDGAR cert deposits, but it pinpoints which entities and which date windows to act on — so a subpoena to the transfer agent or to the DTC / CEDE & Co. depository can pull the certificate-level records that EDGAR never shows, at the moment they matter. It turns a firehose of filings into a short, dated, prioritized watchlist. Precrime flags the factory; the targeted subpoena retrieves the final sale.

score(e) = Σh∈H wh · 𝟙[ h fires on e ] wh ∈ {2, 3}

flag(e) = 1 ⟺ nsig(e) ≥ 2 ∧ score(e) ≥ τ (τ = 3)

16 heuristics (name-recycling, shell-reactivation, reverse-merger chain, filer-agent overlap, going-dark blackout, Reg-S issuance, opinion-letter, calibrated sub-5% positions …) each cast a weighted vote; a lone signal is never flagged. Max score 38. On the model's validation set it fired a mean of 6.6 years before any public action. The same heuristics would have surfaced Davi Skin by 2004 and LATI as early as 1996 — years before the 2007 dump. No enforcement has ever followed against either.

The complete model, the entity genealogy, the per-case findings for both Cane CIKs, and the related accessions are combined on a single companion page:

Structural scoring of SEC EDGAR submissions · forward signal, not an adjudicated finding

Certificate 5304 (5 Mar 2007) deposited 946,085 shares — 16% of Davi Skin's float — nearly doubling the entire 490,096-share non-enterprise pool in a single deposit. No outside party held enough stock to source it; the only candidate is the 85.7% Cane family bloc.

29 days later (3 Apr 2007), certs 5309–5312 sent 2,295,388 shares to four LOM Bermuda nominees at 3.97% each. Combined enterprise control: 4,545,213 sh = 76.69% of free float, ~89% of trading volume. Liquidated for $6,385,033 into Bank of Bermuda (1010-956504) and N.T. Butterfield (20.006.840.351501.100).

In the Jan–Nov 2008 DAVN window the model flagged 11 volume dislocations and 1 confirmed control event; the registration was REVOKED 27 Aug 2012. Despite ~310 EDGAR filings and 40 SOX certifications across the two CIKs, no Wells notice, indictment, or judgment ever issued — instead, Cane obtained a $4,888,924.78 default judgment against the relator.

Court order In re Michael Allan Cane, No. D308221, Dept. E, Eighth Judicial District Court, Clark County, Nevada — Michael Allan Cane → Kyleen Elisabeth Cane (legal name and gender), with Cane appearing as her own counsel.

This 25 Nov 2003 order is the actual change date. The 28 Jun 2001 date Cane later reported to the SEC is roughly 880 days earlier — the backdating that severs the controlling owner from the contemporaneous record and is wired to EDGAR twice (Form 5, then Form 4), each a §1343 wire.

01

The Transformation Pipeline

Now start at the beginning. You've seen the terminal dump and how the certificates were placed; the rest of this report goes back to the start and walks the chain that produced it, one hop at a time. Follow the stock. The scheme begins by concealing who controls a private company — Tele-Lawyer, where the Cane family held the equity outside any SEC scrutiny. When that private stock is taken public, control is split across the family in a Family Bloc — five same-day SC 13G filings (18 Jun 2001). Each holder was individually over 5% (Cane 48.7%, Shirley Cane ~5.35%, the Mekelburgs ~31.65%) and disclosed that stake — but the filings concealed that the five were one coordinated group under Cane, a §13(d)(3) group that together held 85.7% and was required to file as a bloc. From there the same shares are walked through a chain of shells — Dynamic, MW Medical, and finally Davi Skin, the terminal entity: the public listing where the laundered stock is pumped and dumped and the proceeds routed offshore. Read the diagram below as that journey, hop by hop.

Each transformation moved the same insider stock one step closer to a tradeable, liquidatable asset — while the controlling identity was concealed at every hop. The reporting CIK travels intact from MW Medical through Davi Skin (CIK 1059577), so a single hidden shareholder register survives four corporate re-skins. The public listing itself was acquired through a blank-check shell carrying CIK 878146.

Private Nevada incorporation. Cane is sole officer; stock issued to herself and family entirely outside SEC scrutiny — the seed position the entire pipeline exists to monetize.

Dynamic → Legal Access Tech.12 Jun 2001 · CIK 878146

Tele-Lawyer reverse-merges into Dynamic Associates (SIC 6770 blank-check shell); renamed LATI. A 153:1 reverse split wipes out 99.35% of the public float; 5,354,997 shares (91.6%) land with the Tele-Lawyer holders — the public listing the family stock now rides.2

Reverse merger · public listing acquired8-K/Adetail

5 × 13G, same day

3

Family Bloc — stock issued to Cane18 Jun 2001

Cane's own issuance: the Schedule 13D reporting Cane's 48.7% (2,871,051 sh) of the shell, signed "Michael A. Cane."3 On the same date, five Schedule 13G filings — Cane plus Shirley Cane and the Mekelburg bloc — brought coordinated family control to 85.7%, never aggregated or disclosed as a group.5See the five same-day filings

The reporting shell Dynamic spun out 1-for-1 to its holders — so its register mirrors Dynamic's and the family stock rides in through it. (Distributed 11 Mar 1998, before the Tele-Lawyer merger; the lineage, not the calendar, is what carries the stock.) Wallace CEO; counsel signs as "Michael A. Cane." Healthcare ops (Genesis, $49.3M Medicare) supply a commercial veneer.6

MW Medical — Chapter 1122 Jan 2002 → plan 28 Jun 2002

Wallace engineers a sole-secured-creditor position over all assets, then converts debt to equity: 74,000,000 shares at $0.005 (74.1%) under the confirmed Joint Plan of Reorganization.12 A 1:500 reverse split resets the float. Outside equity is extinguished through the bankruptcy.11

Bankruptcy weaponized · In re MW Medical, 02-bk-01090 (Bankr. D. Ariz.)Ch. 11 Plandetail

The reorganized MW Medical shell is rebranded a skincare company — the CIK carries straight through. Wallace CEO, Cane Director, Sim CFO. A legitimate-looking venture (Medley / Mondavi capital) becomes the terminal liquidation vehicle.

The planted seed behind step 4 — the five same-day family filings that split 85.7% control into individually-disclosed stakes — is laid out up top in First, the Stock Is Planted .

The frame emails — manufacturing a paper trail during the dump

As the Davi Skin stock was placed offshore, Cane and Wallace built a paper trail tying outsiders to the nominee structure — so that if the offshore block were ever traced, the names on the paperwork would not be theirs. Three emails fix the method, each opening its source document: 75 the Hepburn Holdings / Bermuda due-diligence package (Gunther → M.P., 23 Apr 2007); 76 Wallace's Social-Security-number request on a MetaWallet/Millicom tender pretext, routed to Cane the next day (11–12 Sep 2007); and 77 the consulting-agreement pretext to assign 556,000 shares to K.G. "to issue shares from transfer agent" (14 Jul 2008). These are laid out by date, with the offshore placements, in the anomaly timeline .

Two operators, one enterprise — and the marks

Every entity from Dynamic to Davi Skin, and the SDI / Galaxy Gaming permutations, sat under the control of Kyleen Cane — the architect and kingpin. As the securities attorney, Cane alone held the legal authority and the expertise to build the scheme: she was counsel, beneficial owner, director, and EDGAR filer, and she dictated each corporate step. Jan Wallace was her agent and instrument — installed as CEO and the manufactured sole secured creditor to front the entities and execute the bankruptcies, but without the sophistication or the authority that only the lawyer commanded. They acted together at every hop — Cane directing, Wallace executing — and at times secretly: the outside names brought in for cover — Parrish Medley and Carlo Mondavi at Davi Skin, shell purchasers such as Beardmore ($250K for MW Asia) — were marks, unaware they were fronting or buying a vehicle already hollowed out and pre-positioned for liquidation. The same playbook that perfected the takeover then obscured the evidence: a backdated identity to sever the trail, CEDE & Co. to anonymize ownership, a bankruptcy to extinguish the shareholders who might ask questions, and a filing-agent switch as the dump began. The same machinery recurs in the related schemes, in chronological sequence — the Wallace identity infrastructure (from 1981), the Thomas & Wong attorney-escrow loan fraud (2002), United States v. DiScala (2012–2018), and the “Voters for Hillary” SuperPAC (2014). Every one of these threads is pleaded together in the filed qui tam complaint — United States ex rel. Phillips v. Cane et al., No. 1:26-CV-21948-LFL (S.D. Fla.).

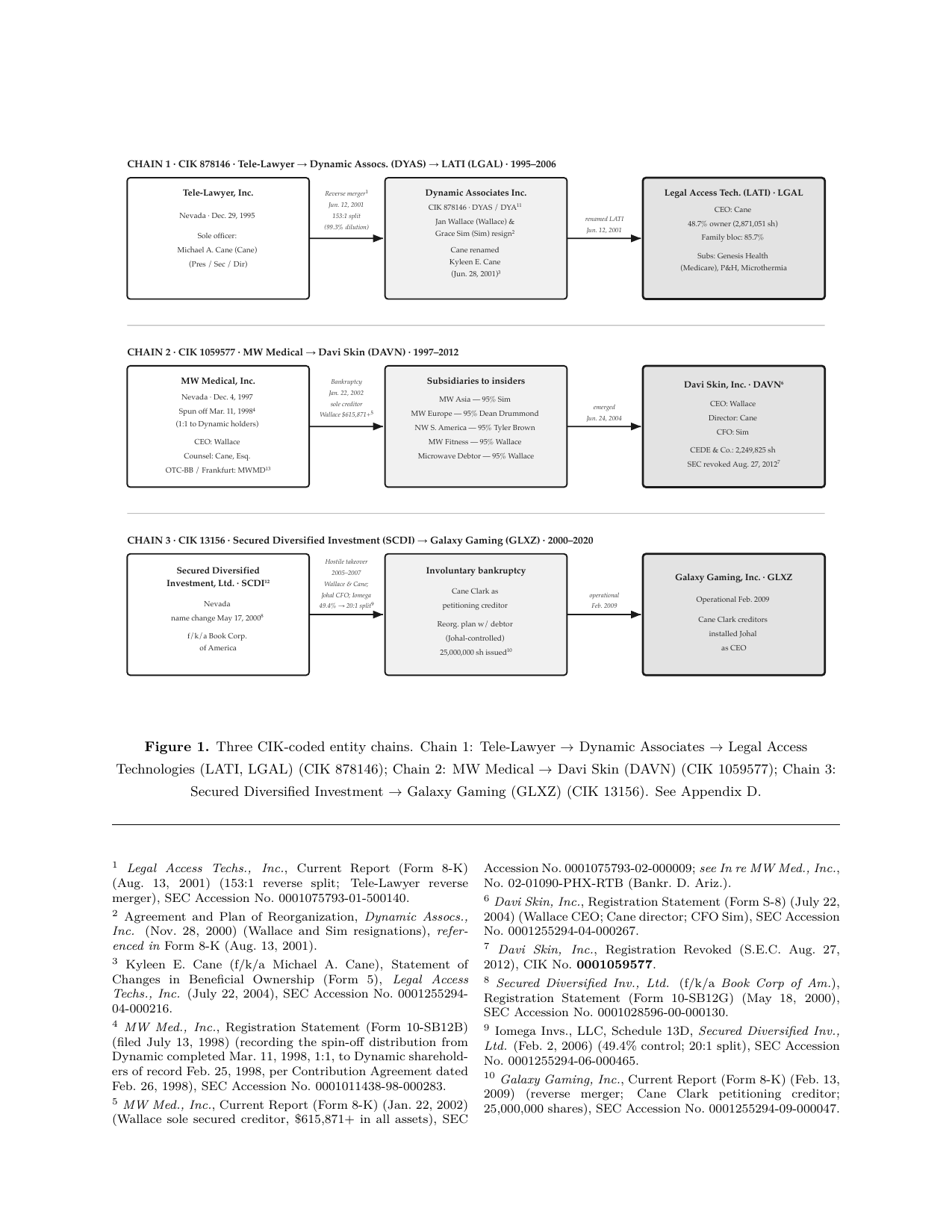

The static companion to the animated pipeline above — the whole enterprise on one page. The scheme resolves into three CIK-coded entity chains (CIK 878146 · CIK 1059577 · CIK 13156), each a corporate lineage that carried the same insider stock forward under a new name. Click either panel to open the source figure71, or open the animated pipeline figure in its own tab.

Read the diagram as genealogy, not a org-chart. A company on EDGAR is identified by a permanent CIK — a number that survives every rename, reverse split, and reverse merger. The scheme exploits that permanence: Chain 1 (CIK 878146) runs Tele-Lawyer → Dynamic Associates → Legal Access Technologies (LATI) — a private Cane-family company reverse-merged into a blank-check shell so the family's stock inherits a public listing. Chain 2 (CIK 1059577) runs MW Medical → Davi Skin — one reporting shell, spun from Dynamic by a 1:1 distribution that mirrors the shareholder register, then re-skinned into the terminal pump-and-dump vehicle. Chain 3 (CIK 13156) runs Secured Diversified Investment → Galaxy Gaming — the same operators recycling a second shell. Because the CIK travels intact, a single hidden shareholder register survives four corporate re-skins: the public-facing name changes, but the concentrated insider ownership underneath does not.

The concealed certificate trail — from private stock to offshore street name

Follow the certificates, not the names. The genealogy exists to move one block of insider stock from a private company nobody could scrutinize into anonymous, free-trading, liquidatable shares — while erasing where it came from at every hop. (1) Origin: Tele-Lawyer issues stock to Cane and family entirely outside SEC scrutiny — the seed position. (2) Public listing: the reverse merger into Dynamic and a 153:1 reverse split wipe 99.35% of the outside float, landing 91.6% with the Tele-Lawyer holders. (3) Group concealment: five same-day Schedule 13G filings (18 Jun 2001) split coordinated family control — 85.7% — into individually-disclosed stakes that were never aggregated as the §13(d)(3) group they were.5 (4) Reconcentration: the MW Medical Chapter 11 converts a Wallace-held note to 74,000,000 shares (74.1%) and extinguishes the outside equity that might ask questions.12 (5) Offshore placement: at Davi Skin a concealed $200,000 note is converted to 2,295,388 shares (15.9%) in four equal blocks to the LOM Bermuda nominees (certs 5309–5312), and 36 sequential CEDE & Co. certificate deposits move 2,249,825 shares into anonymous street name for liquidation offshore.38 Each step severs the certificate from its prior-entity provenance — the very thing the diagram reassembles.

Why shell cycling matters

The re-skinning is not cosmetic — it is the laundering mechanism itself. Every cycle does three things at once: it resets the float (a reverse split erases the outside holders on paper), it launders provenance (a new name and ticker detach today's shares from the fraud that created them), and — through an engineered bankruptcy — it extinguishes the outside shareholders who could testify to what happened. What emerges each time looks like a clean company with a new story, while the concentrated insider block rides the permanent CIK forward, one step closer to tradeable offshore cash. That is why the genealogy is the case: prove the lineage and the "unrelated" Bermuda nominees, the "clean" post-bankruptcy shell, and the "new" public company all resolve back to the same private Cane-family stock. The full narrative is pleaded in the qui tam complaint; the entity roster and CIK cross-reference sit on the EDGAR entities page .

02

Three Names, One Office — and a Family Built to Hide One Person

One person — admitted to the California Bar in 1979 as Michael A. Cane (No. 87106) — has used three legal names and, in Nevada, a separate professional name (Bar No. 5900). The change to "Kyleen E. Cane" was reported to the SEC as effective 28 Jun 2001, sixteen days after the reverse merger; it actually occurred by court order on 25 Nov 200326 and was recorded in Nov 2004.27 From 2019 to 2023 the "Cane" and "Castro" names ran concurrently from a single Las Vegas office (3273 E Warm Springs Rd), selected by forum — Castro to the Secretary of State, Cane to the courts. The backdated date was wired to EDGAR twice, each transmission a discrete wire-fraud act under 18 U.S.C. §1343.24

Michael A. Cane

1979 — 2003

Cal. Bar No. 87106. Reverse-merger counsel and EDGAR filing agent (filer 0001255294). The identity that performed the foundational conduct.

Kyleen E. Cane

claimed 2001 / actual 2003 →

Nev. Bar No. 5900. The identity named in the DOJ indictment United States v. DiScala (E.D.N.Y.)43 and the civil RICO complaints.

K. E. Castro

2019 →

Used to form and maintain Nevada LLCs from the same office. The same person authored a 2024 UC Irvine Ph.D. dissertation as "Kyleen Elisabeth Castro."30

One document carries the through-line: the same career history — B.A. U.C. Irvine 1975, USC J.D. 1978 (Order of the Coif), the Tele-Lawyer / Legal Access Technologies companies, the 2024 U.C. Irvine Ph.D. — repeated verbatim from "Michael A. Cane" to "Kyleen E. Cane" to "Kyleen Elisabeth Castro." Page through all seven; the descriptions map each page.

1Biographies (1 of 2) — “Michael A. Cane” vs “Kyleen E. Cane” (2001) Las Vegas Gaming director bios: same degrees, honors, companies.

2Biographies (2 of 2) — “Kyleen E. Cane” (2001) vs “Kyleen Elisabeth Castro” (2024 U.C. Irvine Ph.D. CV): the same credentials again.

3Credential-overlap table — every distinctive credential (B.A. U.C. Irvine 1975; J.D. USC 1978, Order of the Coif) recurs across all three names.

4The universe of Cane-controlled firms — the law-firm continuum (Wellman & Cane → Cane & Company …) at one Las Vegas address cluster.

5Identity field/value table — legal names, date of birth, California Bar No. 87106, other bar memberships.

6Composite forensic CV — Castro f/k/a Cane f/k/a Michael Allan Cane; concurrent Cane/Castro use 2019–2023 from one office; DOB Oct 22, 1954.

7Concurrent-use detail — Westward Law (2019) & DKM Development (2021) as “K E Castro”; World Series of Golf (2019) & the 2023 renewal affidavit as “Kyleen E. Cane.”

How the family concealed a single controlling person

The 85.7% family bloc was never filed as a group. Splitting one control position across related holders kept every individual filing under an aggregation trigger, so no Schedule 13D "group" was ever declared and the controlling person stayed invisible across the whole chain.

Kyleen E. Cane

self · principal

48.7%

2,871,051 sh

Shirley Cane

mother

~5.35%

family holder

Mekelburg bloc

extended family

~31.65%

coordinated

85.7%

Coordinated family control of LATI / Davi Skin — Cane 48.7% + Shirley Cane ~5.35% + Mekelburg ~31.65% — held in pieces, never aggregated in any SEC filing. Each piece sits under a disclosure line; together they are a single voting bloc.5

The backdated identity, in sequence

03 JUL 1979

Admitted as "Michael A. Cane"

California Bar No. 87106 — the same membership record now reads "Kyleen Elisabeth Cane." A USC J.D. (1978, Order of the Coif) carried verbatim across every later name.29

Bar Record

12 JUN 2001

Reverse merger executed — as Michael A. Cane

Tele-Lawyer into Dynamic / LATI. The foundational securities transaction is performed under the Michael identity.3

SC 13D

28 JUN 2001 — CLAIMED

Reported name change to "Kyleen E. Cane"

The effective date later reported to the SEC — 16 days after the merger, and roughly 2.5 years before the actual court order.

backdated · not disclosed for 1,120 days

DEC 2002 – SEP 2003

Six LATI SOX certifications — "Michael A. Cane"

§302 / §906 certifications signed under the former identity, +533 to +809 days after the claimed change. SOX certs carry criminal liability under 18 U.S.C. §1350.28

10-KSB / SOX

25 AUG 2003

Buys a home as "Michael A. Cane"

15 Quail Hollow Drive, Henderson NV — $575,000, purchased under the Michael identity more than two years after the claimed change and three months before the actual order.

still "Michael" in 2003

25 NOV 2003 — ACTUAL

Court order changes name & gender

In re Michael Allan Cane, Case No. D308221, Dept. E (8th Jud. Dist. Ct., Clark County) — Michael Allan → Kyleen Elisabeth. Cane appeared as her own counsel, "Michael A. Cane, Esq., Bar No. 5900."26

Court Order

22 JUL 2004

Form 5 wired to EDGAR — backdated date

First SEC filing as "Kyleen E. Cane" carries the false June 2001 effective date (+1,120 days). An interstate wire transmission of a false statement — a §1343 predicate.24

Form 5

05 NOV 2004

Form 4 re-transmits the backdated identity

Signed "/s/ Kyleen Cane" and uploaded to EDGAR four days before the 2003 order was recorded (9 Nov 2004) — a second, independent §1343 wire.25

Form 4

24 MAY 2019

"K E Castro" appears — Westward Law, LLC

Nevada annual list filed as Manager "K E Castro" at 3273 E Warm Springs Rd — the earliest Castro filing of record. The concurrency begins.33

NV Annual List

04 JUN 2019

"Kyleen Cane" — World Series of Golf, LLC

Eleven days after the Castro filing, an annual list filed as "Kyleen Cane" — same office, different name.32

11 days apart · same addressNV Annual List

10 APR 2023

Sworn affidavit as "Kyleen E. Cane"

Renews a $4,888,924.78 judgment in Cane v. Phillips (No. A-16-743194-C); served by certified mail and filed electronically — mail (§1341) and wire (§1343) transmissions, sworn as Cane while Castro was active at the Secretary of State.44

mail + wire · Bar No. 5900Affidavit of Renewal

~2.5 yrs

The reported name-change date (28 Jun 2001) predates the actual court order (25 Nov 2003) by roughly two and a half years. Cane bought a home as "Michael A. Cane" in Aug 2003 and signed six LATI SOX certs as Michael through Sep 2003 — then wired the backdated date to EDGAR twice in 2004, each an independent §1343 predicate.

Efforts to conceal: litigation weaponized by forum-selected identity

Cane used two Nevada civil actions as cover and intimidation, filing and swearing as "Kyleen E. Cane" in court while simultaneously operating as "K E Castro" before the Secretary of State — a deliberate split that keeps the two paper trails from being joined.

Cane v. Dhillon

No. A-11-648485-C

filed 16 Sep 2011 · against the firm representing Phillips72

Cane v. Phillips

No. A-16-743194-C

filed 6 Sep 2016 — $4.8M default judgment (19 Jun 2017)45 entered while Cane was on federal pretrial release in U.S. v. DiScala (EDNY)42

The concealment reaches the household. Susan Eiselman — Cane's wife — has continued to live with Cane through the 2003 gender change and after; the 2004 transfer of the marital home, papered as a divorce settlement, functioned as a way to move assets around — splitting and shielding them while the property stayed under Cane's control — rather than an actual separation.

concurrent use · one office · 3273 e warm springs rd, las vegas nv 89120

filed as "K E Castro"

entity formation

Westward Law LLC (24 May 2019) · DKM Development LLC (16 Aug 2021)33

sworn as "Kyleen E. Cane"

litigation & oath

World Series of Golf LLC (4 Jun 2019) · affidavit, Cane v. Phillips (10 Apr 2023)32

Source: Cal. Bar No. 87106 · Nev. Bar No. 5900 · Clark County D308221 / Doc. 20041109:001972 · SEC EDGAR Acc. 0001255294-04-000216 & -000300 · NV SOS SilverFlume

03

What Regulators Saw vs. Reality

Every position was tuned to sit one notch under a disclosure line: 48.7% under the 50% control threshold; family kept un-aggregated; offshore nominees each under the 5% Schedule 13D trigger. The gaps are too precise to be accidental.

ownership_concealment · davi skin / lati — % of voting stock

reported — cane (sec)

48.7%

actual — family bloc

85.7%

enterprise (+ wallace/sim)

89.9%

public float (left over)

10.1%

dashed line = 50% control threshold

37×

Reported individual ownership (48.7%) understated the real coordinated family position (85.7%) by 37 points — the gap that kept a single controlling person invisible across the entire transformation chain.5

Source: 5 Schedule 13G filings, 18 Jun 2001 · Pacific Stock Transfer reports

04

The Calibrated Bermuda Nominees

On 3 Apr 2007, certificates 5309–5312 issued exactly573,847 shares to four entities at one address — The LOM Building, 27 Reid Street, Hamilton. Each lands at 3.97%: just under the 5% reporting trigger. Identical share counts across four "unrelated" foreign entities do not occur in natural markets.

lom_nominee_calibration · each position vs. 5% schedule 13d threshold

arch ltd. — 5309

3.97%

hepburn holdings — 5310

3.97%

the chloe group — 5311

3.97%

sunshine ltd. — 5312

3.97%

dashed line = 5.00% disclosure trigger · bars scaled to threshold

Combined concealed beneficial ownership across the four LOM nominees — 2,295,388 shares — held through LOM Securities (Lines Overseas Management), later charged by the SEC for exactly this nominee-laundering model (SEC v. Lines, 07-cv-11566, SDNY).41

threshold_calibration · each position vs. its disclosure trigger

Cane sits at 97.4% of the 50% control line; each LOM nominee at 79.4% of the 5% Schedule 13D trigger. Every position calibrated just under.

Source: Pacific Stock Transfer, Active Shareholder Report, 13 Jul 200738

05

The Certificate Trail

36 sequential CEDE & Co. certificates deposited 2,249,825 shares into DTC over three years. Deposits accelerate into the 2007 promotional window — 70.6% of all volume — synchronized to the offshore nominee issuance.

cede_deposit_phases · shares deposited to dtc street name, by year

2004 jun–dec · 3 certs

21,950

2005 mar–dec · 9 certs

254,051

2006 feb–nov · 14 certs

385,439

2007 jan–jun · 10 certs

1,588,385

bars scaled to peak year · cert range 2029–5323

cumulative_deposits · shares into DTC street name, 2004–2007

36 sequential CEDE & Co. certificates · 70.6% of all volume lands in the 2007 window; a single certificate (No. 5304) is the near-vertical step.

946,085

A single certificate — No. 5304, deposited 5 Mar 2007 — moved 946,085 shares, nearly double the entire non-enterprise shareholder pool and impossible from any retail source. 29 days later, certs 5309–5312 went to Bermuda. Of 2,249,825 shares deposited, only 335,960 remained by Jul 2007 — 85.1% sold through the CEDE & Co. / DTC street-name channel.38

The shells were not empty husks chosen at random — each iteration wrapped itself around a stream of federal funds to manufacture legitimacy. Medicare billings gave the reporting shell a commercial story; later vehicles in the same orbit drew pandemic relief. Federal money was the veneer that made a laundering pipeline look like a business.

$49.3M

Medicare billings — Genesis Health Mgmt, via Dynamic / LATI (CIK 878146)6

$4.8M

CARES Act / pandemic relief drawn in the SDI → Galaxy Gaming orbit (CIK 13156)

$6.39M

Securities proceeds liquidated through Davi Skin (CIK 1059577)

Genesis Health Management operated up to 26 geropsychiatric hospital units across four states (Louisiana, Arkansas, Mississippi, Tennessee) with 100% of operating revenue derived from Medicare billings — a real federal-payer footprint bolted onto a shell whose only purpose was to host a hidden share register.6 The same playbook — public shell + federal-money story — recurs in the Secure Diversified Investment chain.35

Source: Dynamic / LATI 10-KSB filings (Genesis / Medicare) · SDI internal memoranda & bankruptcy record

07

Offshore Terminus

Davi Skin shares reached the market through two distinct channels. Channel 1 deposited insider stock into CEDE & Co. / DTC street name for sale. Channel 2 converted Wallace's Davi Skin promissory note — the Lahka $200k nominee conversion34 into 2,295,388 shares, issued as certs 5309–5312 and split 4 × 573,847 across the LOM entities. Proceeds settled into the LOM entities' own offshore bank accounts — not a neutral custodian; no FBAR was ever filed and no U.S. capital gain reported. The dump controlled roughly 89% of daily trading volume during the manipulation window.

two channels · one terminus

Channel 1 — CEDE & Co.

DTC street name

2,249,825 sh deposited · 1,913,865 sold (85.1%)

Channel 2 — Wallace note → LOM

Lahka $200k conversion

2,295,388 sh · 4 entities × 573,847 · certs 5309–5312

offshore accounts held by the LOM nominee entities

Proceeds from 2,295,388 shares liquidated through four Bermuda nominees flowed to Bank of Bermuda and N.T. Butterfield. Six mechanisms kept $6.39M off every U.S. return.

1 · Offshore accounts

Proceeds settled directly into Bermuda banks — outside IRS visibility.

2 · No FBARs

Zero FBARs for 21 years; estimated civil penalty exposure exceeds ~$72M.

3 · No capital-gains reporting

No U.S. broker reporting; the sale never appeared on a U.S. tax return.

4 · Reg S fiction

Shares framed as sold to "foreign investors," proceeds argued to belong to foreign entities.

5 · §1145 tax-free spinouts

Subsidiary shells distributed to insiders without registration, sold for $250K–$500K each.

6 · Management-fee laundering

Genesis billed Medicare; fees diverted to structuring entities as "compensation."

$0

U.S. tax reported on $6.39M. Proceeds sat in Bank of Bermuda (1010-956504) and N.T. Butterfield (20.006.840.351501.100); no FBAR, no capital gain, no return.38

09

Wallace Perjury — Bankruptcy Court, 4 Nov 2013

In a sworn deposition during the Galaxy Gaming bankruptcy (CIK 13156), Jan Wallace was examined about offshore accounts.

First — under oath

denial

denied maintaining any foreign bank accounts or offshore assets

Minutes later — same hearing

admission

admitted being signatory / beneficial holder on the Bank of N.T. Butterfield account(s) tied to one or two of the LOM nominees — Hepburn Holdings / Arch Ltd. — i.e., a portion of the proceeds, not the full $6,385,033

Denial then admission in the same proceeding — itself chargeable as perjury (18 U.S.C. §1621) and false declarations (§1623), tying Wallace directly to part of the offshore liquidation proceeds (the Hepburn / Arch LOM accounts).

10

The Patterns, Hiding in Plain Sight

The points below are allegations drawn from the documentary record — they have not been adjudicated. Read that way, the filings still show machine-detectable patterns across EDGAR that are consistent with a coordinated scheme and that anyone with automated detection could surface.

Coordinated 13G filings

Multiple filings on one date, each just below a threshold — a pattern consistent with undisclosed coordination.

Sequential certificates

Sequential numbers point to a single source even where the beneficial owner is not named.

Mathematical calibration

Four identical share counts (573,847 × 4) are highly improbable as independent market activity.

Bankruptcy-to-trading

A bankruptcy that extinguishes outside equity, followed immediately by share deposits — a sequence the record reflects.

~650

Analysis of ~24M SEC accessions reportedly surfaces roughly 650 similar entity clusters sharing the same signatures — same registered agent, incorporator, address, banks, nominee patterns. The Cane case reads as a template, not an anomaly.(analysis, not a primary-document finding)

11

Why No Regulator Caught This

Institutional fragmentation. SEC, IRS, FinCEN, and state regulators each see fragments; none has full visibility.

Filing volume. Millions of filings a year; without pattern detection, anomalies are invisible.

Legal sophistication. An attorney designed structures to exploit the seams between securities, bankruptcy, and tax law.

Offshore routing. Bermuda nominees and accounts provide legal obscurity even when domestic activity is flagged.

Network connections. Associations alleged in offshore-leak datasets suggest infrastructure beyond a single fraud. (allegation/analysis)

12

Federal Laws, SEC Rules & Crimes

The documentary record implicates the following — every entry maps to conduct shown above.

Wire fraud — electronic transfer of $6.4M offshore via the DTC/CEDE nominee system; backdated identity wired to EDGAR

18 U.S.C. §1341

Mail fraud — SEC filings and sworn affidavits with material misrepresentations sent through the mails

18 U.S.C. §1956 / §1957

Money laundering — $6,385,033 routed through four Bermuda nominees into Bank of Bermuda and N.T. Butterfield

31 U.S.C. §5324

Structuring — four LOM nominees each at exactly 573,847 sh (3.97%), calibrated below the 5% Schedule 13D trigger

18 U.S.C. §1962

RICO — pattern of racketeering through the Cane–Wallace enterprise, 1995–2023

18 U.S.C. §152

Bankruptcy fraud — manufactured sole-secured-creditor position; §1145 abuse to distribute shells to insiders

18 U.S.C. §1347

Healthcare fraud — $49.3M Medicare billing via Genesis; management fees diverted to structuring entities

18 U.S.C. §1621 / §1623

Perjury / false declarations — Wallace testimony (Nov. 4, 2013): denied, then admitted, offshore accounts in one proceeding

26 U.S.C. §7201

Tax evasion — $6,385,033 unreported offshore income; zero FBARs filed for 21 years

SEC Rules 13d-1, 13d-2, 13g-1

Failure to file / falsify Schedule 13D/G — 85.7% family bloc never aggregated; LOM bloc reported as “unrelated third parties”

Statutes & rules implicated by the documentary record · allegations

13

The Full Picture

What appears in SEC filings as routine corporate activity was an engineered pipeline: convert private stock into tradeable shares, concentrate ownership while reporting the opposite, extinguish outside holders through manufactured bankruptcy, and liquidate through calibrated offshore nominees — all below every disclosure threshold.

The mathematical precision — four nominees at exactly 3.97%, a 153:1 split calibrated to exact percentages, 36 sequential certificates from one source — is the signature of design, not coincidence — resting on 28 false SEC filings and 3 false SOX certifications across four CIKs: Dynamic/LATI (878146), MW Medical/Davi Skin (1059577), Sedona Software (1100131), and LVGI (1103993).

The same machinery, other arenas

Davi Skin was not isolated. The same operators ran the same plays — attorney-trust pass-throughs, manufactured creditor positions, offshore nominees, and a legal veneer over operational control — across the other documented arenas, in chronological sequence:

The Wallace identity infrastructure(from 1981) — four aliases and three Social Security numbers (two stolen from the deceased, one fabricated), each assigned a fraud function, with bankruptcy testimony of “no offshore accounts” contradicted by her own prior sworn testimony about Hepburn Holdings (Bermuda): the concealment layer beneath the whole enterprise.57

Genesis Health Management(1994–2001) — the federal-money engine that preceded the share-trafficking: Dynamic Associates billed Medicare directly through the geropsychiatric PPS exemption, generating ~$49.3M in management fees while a convicted Medicaid felon and an OIG-excluded doctor sat inside the controlled group and a Genesis-employee qui tam was disclosed once and then suppressed — with $3.28M of government money routed to offshore Reg S noteholders.60

MW Medical(1998–2004) — the shell Dynamic Associates spun off to its own shareholders in 1998 and Wallace ran, weaponized through a manufactured Chapter 11: a self-dealt secured note placed Wallace first in line, the §1145 plan made the reorganized shares free-trading, and the vehicle re-emerged as Davi Skin.61

Dynamic Associates / LATI(2001) — the blank-check shell (SIC 6770) reverse-merged into Legal Access Technologies: roughly $8.6M of noteholder debt converted to stock and a 153:1 reverse split handed the Cane family bloc ~91.6% of the float while the offshore pre-merger holders were diluted to near zero.62

Thomas & Wong(2002) — off the $250K sale of the MW Asia shell to Beardmore, Wallace induced a contractor to wire $1.5M into a Cane O'Neill attorney trust account for a bridge loan; three unauthorized diversions ran before any documents were signed and the gold-doré collateral never existed, yielding a $1.3M non-dischargeable judgment.57

SDI / Galaxy Gaming(2005–2008) — the same takeover-by-bankruptcy on Secured Diversified Investment: Cane Clark appeared as a petitioning creditor against its own client, an involuntary Chapter 11 and a 20:1 reverse split concentrated control, and the clean public shell was delivered to Galaxy Gaming holders.58

United States v. DiScala(2012–2018) — the only federal indictment naming Cane directly (E.D.N.Y., 2014): she held millions of free-trading shares in attorney escrow and released them on trading instructions across four shells generating $300M in artificial market cap. A 2014 wiretap caught her on price control; she was acquitted at the 2018 trial.55

The “Voters for Hillary” SuperPAC(2014) — formed 17 days before her indictment was unsealed, with Cane lending it $10,700. The PAC funneled $73,000 to CrossClick Media (XCLK) — a Cane Clark client penny stock — while PAC insiders controlled CrossClick: the same circular share-control structure in a campaign-finance wrapper.56

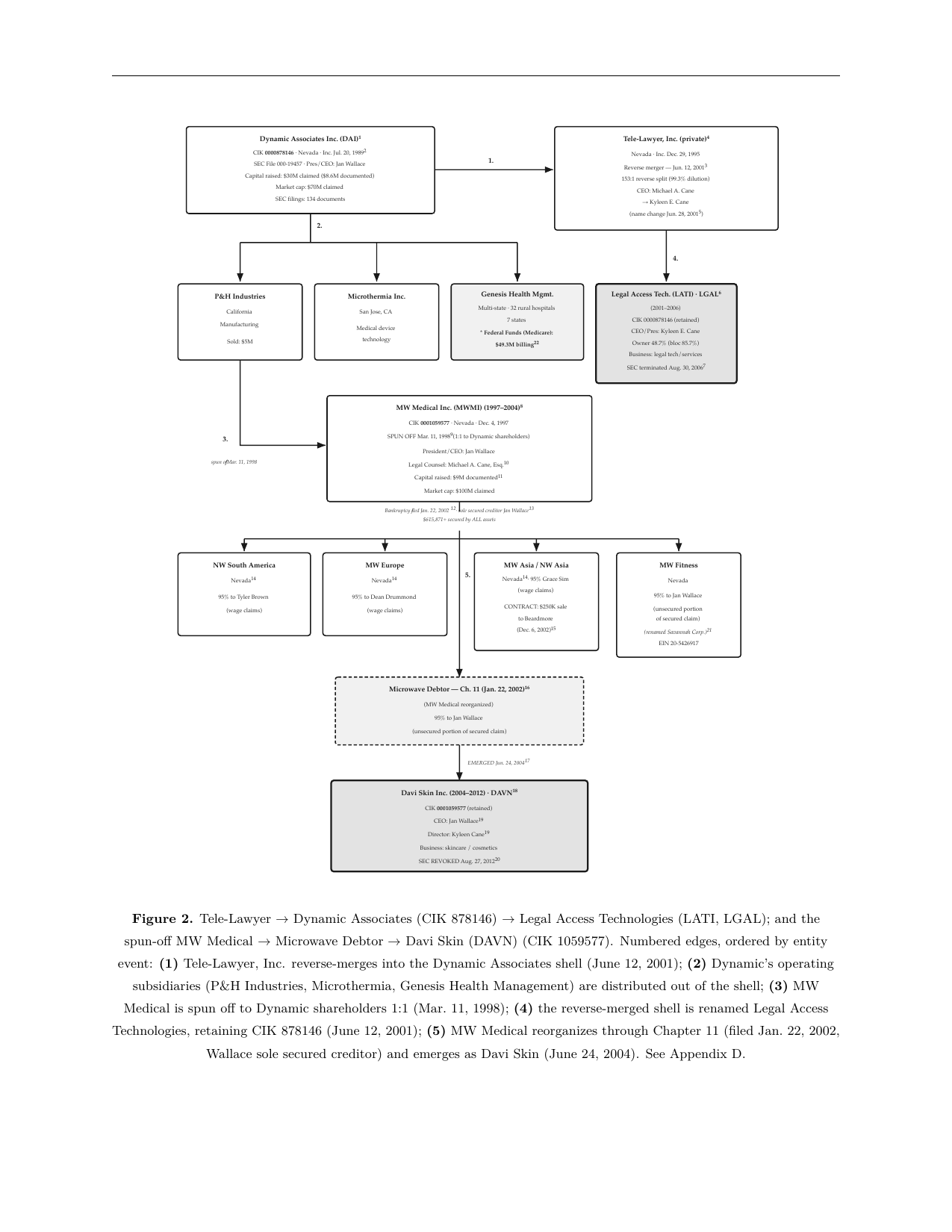

Tele-Lawyer, Inc. was Kyleen Cane's private Nevada corporation — the origin point of the scheme. It had no public market and its shares had no liquidity.

By merging it into the already-public Dynamic Associates on 12 Jun 2001, Cane converted worthless private stock into a publicly registered position with a CUSIP, without an IPO. Dynamic itself (incorporated 20 Jul 1989, SIC 6770 blank-check) claimed $30M raised but documented only $8.6M, and filed 134 SEC documents while running no commercial operations — a parking structure awaiting a reverse merger.

MW Medical, Inc. (CIK 1059577) was incorporated 4 Dec 1997 and spun out of Dynamic on 11 Mar 1998 by a 1:1 distribution14. CEO Jan Wallace; counsel signed as "Michael A. Cane."

Its commercial veneer was real federal money: Genesis Health Management ran up to 26 geropsychiatric hospital units across four states (LA, AR, MS, TN), billing roughly $2M/quarter — about $49.3M in Medicare, ~100% of operating revenue6. Management fees flowed to Cane-affiliated structuring entities. Other subsidiaries: P&H Industries (sold ~$5M) and Microthermia Inc.

The 12 Jun 2001 reverse merger renamed Dynamic to Legal Access Technologies, Inc. (LATI)2. A 153:1 reverse split wiped out 99.35% of the public float4.

The split was calibrated to produce exact family-bloc percentages: 5,354,997 shares (91.6%) landed with the Tele-Lawyer holders. CIK 878146 carries the predecessor shell forward intact.

After the merger, five "independent" reporting persons filed for LATI within 24 hours — Kyleen/Michael Cane 48.7%, mother Shirley Cane, and the Mekelburg holders — a coordinated bloc reaching 85.7% that was never aggregated or disclosed as a group.

Each filing sat below a disclosure line; three "unrelated" holders reported the identical 312,500-share block; all five were submitted by one EDGAR filer (0001075793, Cane Clark) on the same 18 Jun 2001 event date5. See the evidence table in this section.

On 22 Jan 2002 MW Medical filed a Chapter 11 voluntary petition13 (In re MW Medical, Inc., No. 2:02-bk-01090-RTB, Bankr. D. Ariz.)11. Wallace manufactured a $615,871 secured promissory note to become sole secured creditor18.

Under the confirmed Joint Plan of Reorganization12 she converted $375,000 of the note to 74,000,000 shares at $0.005 (74.1%), extinguishing outside equity19. The §1145 exemption then let subsidiary shells (MW Asia/Europe/South America/Fitness) be distributed to insiders without registration — later sold for $250K–$500K each.

MW Medical was rebranded Davi Skin, Inc. with outside investors Parrish Medley and Carlo Mondavi as cover; the CIK carries straight through. A 1-for-500 reverse split concentrated the float.

Wallace then asserted a fictitious $200,000 promissory note — already resolved in the bankruptcy — and on 3 Apr 2007 converted it into 2,295,388 shares routed to four Bermuda nominees, which the 10-KSB described as "unrelated third parties."20

Cane's shares — traced from Dynamic through MW Medical to Davi Skin via the 1:1 spin-off — were placed into CEDE & Co. / DTC street name.

Between Jun 2004 and Jun 2007, 36 sequential certificates (Nos. 2029–5323, 2,249,825 shares) were deposited — 3 certs in 2004, 9 in 2005, 14 in 2006, 10 in 2007. A single certificate, No. 5304, deposited 5 Mar 2007, moved 946,085 shares — 16% of the float in one deposit.

The sequential numbering proves a single controlled source; Wallace showed only 100 shares (cert 5064) on the register, concealing the true position.38

A separate operation, structuring different stock. Wallace asserted a fictitious $200,000 Davi Skin promissory note — already resolved in the bankruptcy — and on 3 Apr 2007 Cane converted it into 2,295,388 shares34, issued as four certificates, 573,847 sh (3.97%) each, to The LOM Building, 27 Reid Street, Hamilton:

Combined 15.88% beneficial ownership, zero Schedule 13D filed. Proceeds (~$6,385,033) settled into the LOM entities' own offshore accounts — Bank of Bermuda 1010-956504 (Arch Ltd.) and N.T. Butterfield 20.006.840.351501.100 (Hepburn Holdings Ltd.).38

Two EDGAR submissions — cached & highlighted

Both submissions are reproduced verbatim from EDGAR, cached with this report. The highlighted lines show the same tell on two distinct filings — a Form 5 (period 30 Apr 2003, filed 22 Jul 2004) and a Form 4 (period 31 Aug 2004, filed 5 Nov 2004) — each carrying the FORMER CONFORMED NAME: CANE MICHAEL A · DATE OF NAME CHANGE: 20010628 header and the /s/ Kyleen Cane signature, yet first entering EDGAR's ownership record only in 2004.

The Schedule 13D filed 5 Jul 2001 (event 26 Jun 2001), reporting Cane's 2,871,051 shares — 48.7% of Legal Access Technologies, and signed “Michael A. Cane.” The issuance-and-control block is highlighted; this is the stock position acquired as Michael, three years before the “Kyleen” identity entered the ownership record.

-----BEGIN PRIVACY-ENHANCED MESSAGE-----

Proc-Type: 2001,MIC-CLEAR

Originator-Name: [email protected]

Originator-Key-Asymmetric:

MFgwCgYEVQgBAQICAf8DSgAwRwJAW2sNKK9AVtBzYZmr6aGjlWyK3XmZv3dTINen

TWSM7vrzLADbmYQaionwg5sDW3P6oaM5D3tdezXMm7z1T+B+twIDAQAB

MIC-Info: RSA-MD5,RSA,

Eb2uznmw83/849mZB0SVfXedUpBldZMheoUfMWDtigJUTH8daTcM5Wl/7GVFgG5j

y2CzUSYawVfWuQLYC26kBw==

<SEC-DOCUMENT>0001075793-01-500095.txt : 20010629

<SEC-HEADER>0001075793-01-500095.hdr.sgml : 20010629

ACCESSION NUMBER: 0001075793-01-500095

CONFORMED SUBMISSION TYPE: SC 13D

PUBLIC DOCUMENT COUNT: 1

FILED AS OF DATE: 20010628

SUBJECT COMPANY:

COMPANY DATA:

COMPANY CONFORMED NAME: LEGAL ACCESS TECHNOLOGIES INC

CENTRAL INDEX KEY: 0000878146

STANDARD INDUSTRIAL CLASSIFICATION: SERVICES-SPECIALTY OUTPATIENT FACILITIES, NEC [8093]

IRS NUMBER: 870473323

STATE OF INCORPORATION: NV

FISCAL YEAR END: 1231

FILING VALUES:

FORM TYPE: SC 13D

SEC ACT:

SEC FILE NUMBER: 005-59267

FILM NUMBER: 1670637

BUSINESS ADDRESS:

STREET 1: C/O CANE & CO

STREET 2: 2300 W SAHARA AVE #500 BOX 18

CITY: LAS VEGAS

STATE: NV

ZIP: 89102

BUSINESS PHONE: 7023126255

MAIL ADDRESS:

STREET 1: C/O CANE & CO

STREET 2: 2300 W SAHARA AVE #500 BOX 18

CITY: LAS VEGAS

STATE: NV

ZIP: 89102

FILED BY:

COMPANY DATA:

COMPANY CONFORMED NAME: CANE MICHAEL A

CENTRAL INDEX KEY: 0001144030

STANDARD INDUSTRIAL CLASSIFICATION: []

FILING VALUES:

FORM TYPE: SC 13D

BUSINESS ADDRESS:

STREET 1: 105 QUAIL RUN ROAD

CITY: HENDERSON

STATE: NV

ZIP: 89014

BUSINESS PHONE: 7023126255

MAIL ADDRESS:

STREET 1: 105 QUAIL RUN ROAD

CITY: HENDERSON

STATE: NV

ZIP: 89014

</SEC-HEADER>

<DOCUMENT>

<TYPE>SC 13D

<SEQUENCE>1

<FILENAME>schthirteeddmac.txt

<TEXT>

<PAGE>

UNITED STATES OMB APPROVAL

SECURITIES AND EXCHANGE COMMISSION OMB Number: 3235-0145

Washington, D.C. 20549 Expires: August 31, 1999

Estimated Average burden

Hours per response...14.90

SCHEDULE 13D

Under the Securities Exchange Act of 1934

(Amendment No. _________)*

LEGAL ACCESS TECHNOLOGIES, INC.

--------------------------------------

(Name of Issuer)

COMMON STOCK, $0.001 PER SHARE PAR VALUE

---------------------------------------------

(Title of Class of Securities)

52464H 10 2

------------

(CUSIP Number)

MICHAEL A. CANE

105 Quail Run Road

Henderson, NV 89014

(702) 312-6252

------------------------------------------------

(Name, Address and Telephone Number of Person

Authorized to Receive Notices and Communications)

JUNE 18, 2001

--------------

(Date of Event Which Requires Filing of this Statement)

If the filing person has previously filed a statement on Schedule 13G

to report the acquisition which is the subject of this Schedule 13D,

and is filing this schedule because of Rule 13d-1(b)(3) or (4), check

the following box [ ].

*The remainder of this cover page shall be filled out for a reporting

person's initial filing on this form with respect to the subject class

of securities, and for any subsequent amendment containing information

which would alter the disclosures provided in a prior cover page.

The information required in the remainder of this cover page shall not

be deemed to be "filed" for the purpose of Section 18 of the

Securities Exchange Act of 1934 ("Act") or otherwise subject to the

liabilities of that section of the Act but shall be subject to all

other provisions of the Act (however, see the Notes).

<PAGE>

CUSIP No. 52464 H 10 2

- --------------------------------------------------------------------------

1. Names of Reporting Persons

I.R.S. Identification Nos. of above persons (entities only).:

MICHAEL A. CANE

- --------------------------------------------------------------------------

2. Check the Appropriate Box if a Member of a Group (See Instructions)

(a) [_]

(b) [ ]

- --------------------------------------------------------------------------

3. SEC Use Only:

- --------------------------------------------------------------------------

4. Source of Funds (See Instruction): PF

- --------------------------------------------------------------------------

5. Check if Disclosure of Legal Proceedings is Required Pursuant to Items

2(d) or 2(e):

- --------------------------------------------------------------------------

6. Citizenship or Place of Organization: U.S.A.

- --------------------------------------------------------------------------

Number of Shares Beneficially by Owned by Each Reporting Person With:

7. Sole Voting Power: 2,871,051 SHARES

--------------------------------------------------------

8. Shared Voting Power: NOT APPLICABLE

--------------------------------------------------------

9. Sole Dispositive Power: 2,871,051 SHARES

--------------------------------------------------------

10. Shared Dispositive Power: NOT APPLICABLE

- --------------------------------------------------------------------------

11. Aggregate Amount Beneficially Owned by Each Reporting Person:

2,871,051 SHARES

12. Check if the Aggregate Amount in Row (11) Excludes Certain Shares

(See Instructions):

NOT APPLICABLE

13. Percent of Class Represented by Amount in Row (11): 48.7%%

- --------------------------------------------------------------------------

14. Type of Reporting Person (See Instructions): IN

- --------------------------------------------------------------------------

- --------------------------------------------------------------------------

Page 2 of 4

<PAGE>

CUSIP No. 52464 H 10 2

- --------------------------------------------------------------------------

ITEM 1. SECURITY AND ISSUER.

The class of equity securities to which this Statement relates is

shares of common stock, par value $0.001 per share (the "Shares"), of

LEGAL ACCESS TECHNOLOGIES, INC., a Nevada Corporation (the

"Company"). The principal executive offices of the Company are

located at 2300 W. Sahara Ave., Suite 500, Box 18, Las Vegas, Nevada

89102

ITEM 2. IDENTITY AND BACKGROUND

A. Name of Person filing this Statement: Michael A. Cane (the "Holder")

B. Residence or Business Address: 105 Quail Run Rd., Henderson,

Nevada 89014

C. Present Principal Occupation and Employment: The Holder is a self-employed

businessman.

D. The Holder has not been convicted in any criminal proceeding (excluding

traffic violations or similar misdemeanors) during the last five years.

E. The Holder has not been a party to any civil proceeding of a judicial

or administrative body of competent jurisdiction where, as a result of

such proceeding, there was or is a judgment, decree or final order

enjoining future violations of, or prohibiting or mandating

activities subject to, federal or state securities laws or finding any

violation with respect to such laws.

F. Citizenship: The Holder is a citizen of the United States of America.

ITEM 3. SOURCE AND AMOUNT OF FUNDS OR OTHER CONSIDERATION.

Shares acquired as part of a merger in a share for share exchange

ITEM 4. PURPOSE OF TRANSACTION

Merger

ITEM 5. INTEREST IN SECURITIES OF THE ISSUER.

A. As of June 11, 2001, the Holder holds beneficially the following

securities of the Company:

Title of Security Amount Percentage of Shares of Common Stock*

- ----------------- --------- -------------------------------------

Common Stock 2,821,051 48.7% (combined)

Options 50,000

- ----------------- --------- -------------------------------------

*calculated in accordance with Rule 13d-3

Page 3 of 4

<PAGE>

CUSIP No. 52464 H 10 2

- --------------------------------------------------------------------------

B. The Holder has the sole power to vote or to direct the vote of

the Shares held by him and has the sole power to dispose or to

direct the disposition of the Shares held by him.

C. Not Applicable

D. Not Applicable.

E. Not Applicable.

ITEM 6. CONTRACTS, ARRANGEMENTS, UNDERSTANDINGS OR RELATIONSHIPS WITH

RESPECT TO SECURITIES OF THE ISSUER.

None.

ITEM 7. MATERIAL TO BE FILED AS EXHIBITS.

None.

SIGNATURE

After reasonable inquiry and to the best of my knowledge and belief, I

certify that the information set forth in this statement is true,

complete and correct.

June 26, 2001

--------------------------

Date

/s/ MICHAEL A. CANE

--------------------------

Signature

MICHAEL A. CANE

BENEFICIAL OWNER

--------------------------

Name/Title

Page 4 of 4

</TEXT>

</DOCUMENT>

</SEC-DOCUMENT>

-----END PRIVACY-ENHANCED MESSAGE-----

{kind=link}

{kind=link}

Figure 1 — three CIK-coded chains · open full PDF

Figure 1 — three CIK-coded chains · open full PDF

Figure 2 — detailed scheme flow · open full PDF

Figure 2 — detailed scheme flow · open full PDF